Community Solar's Bend Toward Energy Justice, Episode Two: Utilities Push Back

In Brief

When we started this inquiry, we spelled out how community-wide solar plans can lift renewables' share and lower energy bills.

Every entrant complicates things for incumbents, though- and entrepreneurs aiming to broaden community-solar developments need to confront its obstacles.

So challenges involving rate-setting, marketing and interconnection can seem to suppress community solar growth- at least, they do with current prevalent market structures.

For those of you who read the first article in this series outlining the potential upside of community solar, welcome back! For the rest of you, I recommend that you read that article first in order to sustain the cautious optimism I intend. The purpose of this article is to outline obstacles to widespread adoption of community solar. Part three will close with possible solutions to the challenges impeding the sector’s development, and a positive note.

Now, as I have learned about community solar, issues relating to utility market regulations, state and local laws, and customer management services have registered with nuance. Perhaps the greatest challenges involve how variable the rules and economics of these projects are, depending on their location. I will try my best to outline the main issues, but observations should be viewed as data points within a broader conversation about the challenges in this sector.

Utilities and Regulators Present Challenges

Foremost among the challenges community solar faces is the regulatory docket. As of May 2021, only 21 states have passed legislation that allows for interconnection and subscription of community solar projects.

Part of the reason for this low adoption rate seems to involve the often-lethargic movement of the legislative process, but stiff opposition from powerful actors likely makes a deeper impact.

During my conversation with Kevin Betz, a project developer for Community Energy, he explained that “while there has been significant growth in the last 10 years, getting new legislation passed and negotiating new regulations can be quite a political challenge.”

Why though would anyone be against opening the market to a compelling solution to energy equity and climate change? Well, it’s complicated, but the short answer is: money.

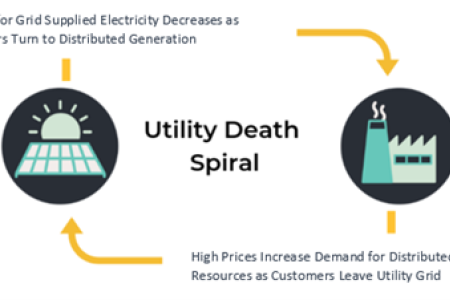

Utilities have invested billions into the transmission and generation assets that currently power America, and many made these investments with the understanding that they were operating in a non-competitive environment with a set customer base. If too many of their customers began using privately-owned distributed energy resources (i.e. community solar), the utilities may need to increase rates on their remaining customer base to support their massive grid infrastructure assets, usually procured using sizable debt. This increase in rates will in turn make the community solar option more appealing and could push more customers to opt out of the utility, which would reinforce this cycle of rate increases. This theoretical scenario earned the name “utility death spiral.” According to a 2017 survey of leaders in the utility industry, over 70% see this outcome as a real possibility in the absence of regulatory intervention. (This diagram from the Power Futures Lab, a nonprofit exploring utility policy at the University of Cape Town Graduate School of Business, gives shape to the fear.)

In addition to state and local complexities, the response from utilities has varied based on whether they are in a regulated or deregulated market. As defined in an article by EnergyWatch, a “regulated electricity market” contains utilities that own and operate all electricity, from the generation to the meter, the utility has complete control. Meanwhile, a “deregulated electricity market” allows for the entrance of competitors to buy and sell electricity by permitting market participants to invest in power plants and transmission lines.

As one might expect, the regulated utilities are more likely to oppose new competition into their market while deregulated utilities are more adapted to competition and have less incentive to exclude solar. This difference is seen in existing regulation as 75% of the 16 states (plus D.C.) that currently have deregulated electricity markets have supportive community solar legislation in place, compared to approximately 25% in the regulated energy markets. Consider how Arizona Public Service utility actively fought against residential solar by spending millions on anti-solar ads to discourage supportive policies and regulations.

Many developers understand the difficult situation that utilities face. During a panel at the Infocast Community Solar 2.0 conference, Rick Hunter, CEO of the community solar development company Pivot Energy Solutions, said that “there is hostility from utilities, and rightly so, because we are taking their customers and they are not getting any credit for enabling this investment in clean energy.” On the other side of the coin, organizations such as the Coalition for Community Solar Access are fighting to pass enabling legislation on behalf of a public that generally doesn’t know the model or its potential benefits.

Whatever its economic calculus, the opposition from utilities presents a major barrier to community solar. In an interview with Quartz, Matt Hargarten, the public affairs director for the Coalition for Community Solar Access (CCSA), argued that the success of the community solar model relies on competition. “There are no technical barriers to community solar,” he says, although he believes utilities have fought hard to exclude rivals. “A robust community solar market requires enabling legislation at the state level.”

Siting and Permitting Issues Are Abundant

Even within the states where utilities and regulations support community solar, there are siting challenges that must be addressed before projects can be built. Betz outlined the key components that determined site suitability: “compliance with the local zoning and permitting requirements, the willingness of a property owner to partner with the developer, and whether the local distribution grid can handle the amount of energy the system will be injecting into the circuit.”

The last point regarding grid capacity and interconnection for community solar projects is crucial. In states where distributive energy resources are becoming prevalent, the challenge of interconnection delays has already translated to meaningful disruption in community solar development and costly fines. Perhaps even more burdensome are the potential upgrades that the developers may have to make to connect to aging or insufficient grid infrastructure. “One of the biggest unknown costs for community solar project developers is whether a project will trigger a substation upgrade or incur other upgrade costs that will render the project unfinanceable,” Laurel Passera, policy director for CCSA, says in the organization's March newsletter.

The Public Utility Regulatory Policies Act (PURPA), passed over 40 years ago, forces the distributed generation project that triggers the need for a grid upgrade to pay for it. This can cost a project millions. In one case, according to an advocate who got her views into the Bangor Daily News, a project in Maine that had already signed a contract and started construction had its interconnection fee increased from $239,000 to $12,239,000.

In addition to the zoning and interconnection issues, developers have to consider the economic and environmental impact of different sites. Rooftop solar benefits from being sited on economically unproductive and environmentally low-impact spaces. The same cannot be said, however, for all community solar (or utility scale solar for that matter), as the projects require a large contiguous parcel of sunny land, preferably near a large population and local substation.

The above image is featured in a Solstice article discussing pros and cons of community and residential solar. The projects can take valuable farmland space.

This can impact the project’s finances, given quoted prices of $2,000 per acre each year for a site near a substation just outside an urban area. While the size of land needed for community solar varies, developer/operator OYA Solar estimates that they need 30 to 40 acres to build 5 MW solar farms with an average lease duration of 25 years, which translates to approximately $1.5-2 million over the project’s lifetime. If the land can be used for agriculture, the costs are even higher as the USDA calculated the average cost for an acre of crop land to be $4,100.

The use of greenfield land for these projects can also have a sizable impact on the environment. In some instances, the site requires land clearing, which can create unintended environmental consequences, from deforestation to habitat loss. The land use pressure will be immense, as NREL estimates that 3 million acres of U.S. land will be absorbed by the solar industry. This has raised concern for many who fear that the land change will disproportionately impact agricultural and BIPOC communities. In an article for E&E News, Rich Holschuh of the not-for-profit Atowi Project, expressed his fears of this possible future. "With the swing in the Biden administration toward green energy and fuel switching, I think the pressure that is going to be brought to bear on forest and farmland is going to be tremendous."

Subscription Management and Bill Pay

So far, the only challenges I have touched on relate to the development of community solar projects. While this creates pain points for most renewable energy projects, community solar also faces unique operational challenges in customer acquisition and management.

Typically, the project developer will enter a contract with a subscription manager who will find eligible subscribers for the project and manage their payments. This system of contracting out the subscription management mirrors how project developers use engineering, procurement and construction (EPC) and operations and maintenance (O&M) contracts to engage experts who manage specific parts of the project. The advantage of these subscription contracts is that similar to the EPC and O&M contracts, they allow the developer to work with a leaner team and the terms of these contracts often pass a significant portion of the subscription management risk onto the contractor in exchange for a higher contract price.

Even still, there is risk in outsourcing this vital component. Inclusive Prosperity Capital (IPC)’s Director of Clean Energy Transactions, John D’Agostino, explained “the professional capacity of the contracted subscriber manager contributes significantly to community solar project’s risk or strength as a performing asset. Subscriber managers’ specific abilities range depending on their experience in a given market or with specific project types or sizes. [Emerging best-in-class players can conduct] proprietary marketing and outreach and cultivated inventory of interested potential subscribers to a given project, [as well as] innovative financing models that de-risk the impact of subscriber turnover and associated bill payments.”

The first issue to consider is customer acquisition. A variety of methods, from telemarketing to door-knocking, helps firms find eligible subscribers, and customer acquisition accounts for up to 5% of the total project cost. With this high cost in mind, there is an incentive to have long-term customers which can obstruct the sector’s ability to provide cheap clean energy to people who rent. Renters have much higher moving rates, estimated to be nearly four times higher than homeowner rates at 22% in 2017, so developers face higher customer turnover costs when they target renters.

There is an incentive to have long-term customers which can obstruct the sector’s ability to provide cheap clean energy to people who rent.

People with low or moderate incomes also have, on average, lower credit scores which have historically excluded them from the residential solar market. These credit scores also complicate participation in community solar (albeit to a lesser extent) as some developers impose a minimum threshold score of 650 or higher, according to Steph Speirs, the Solstice CEO and co-founder. However, a study by the Federal Reserve in 2018 showed that the average credit score for people making less than $30,000 a year was well short of this threshold at 590. This restriction may be ill-advised. Speirs noted in an interview with Greentech Media that “FICO doesn’t measure whether you pay your utility bills on time or if you pay your rental or cell phone bills on time [and] it is an imperfect proxy for whether you should qualify for community solar.”

There are also frequent issues in the billing process, as utilities and project owners adapt to the pass-through payment system. Developer and utility often stumble as they reconcile their information to ensure that the customer is paying the correct amount. The issue, as observed in Solar Builder Mag by asset manager Will Jurith, flows from extra meters. “There is one meter installed at the project and then another at the utility—and those two rarely, if ever, match up exactly at the end of each month.” Also, the customer may receive two separate bills from the utility and the project. This does not inherently increase prices for the subscriber, but who needs more bills? Finally, updating an existing utility billing system to accommodate community solar participation can, according to the Smart Energy Power Alliance (SEPA), cost upwards of $1 million and require the work of dozens of employees to make the change.

Well, I hate to leave things on a sour note, but for those who found this article to be frustrating or discouraging, hopefully in a few weeks’ time I can assuage your concerns. The challenges facing community solar are substantial, however, they are by no mean insurmountable. In the final article in this series I will lay out some of the proposed solutions.